India’s digital payments ecosystem runs heavily on UPI payment systems. Millions of transactions happen every minute. But there has always been one small challenge — small-value transactions sometimes fail or take longer to process, especially during peak hours.

Think about paying ₹20 for tea or ₹50 for parking. These micro payments often compete with larger UPI payment transactions on the same banking infrastructure. That is exactly the problem UPI Lite was designed to solve.

UPI Lite is a lightweight payment feature that allows you to make instant small-value digital payments without entering your UPI PIN every time.

In simple terms, UPI Lite offers:

- No UPI PIN required for payments

- No additional KYC required

- Faster payments for small transactions

- Optional offline mode support

- A transaction limit of ₹1,000 per payment

With UPI Lite, everyday purchases become faster, smoother, and more reliable — helping India move closer to truly seamless cashless payments.

Table of Contents

What Is UPI Lite?

UPI Lite is an on-device wallet embedded within your UPI app. Unlike regular UPI payments, which route every transaction through your bank’s server in real-time, UPI Lite stores a small amount of money directly on your phone. When you pay, the transaction is processed locally, which makes it significantly faster and far less prone to failure.

It was designed and launched by NPCI (National Payments Corporation of India) to reduce the load on banking infrastructure caused by the sheer volume of low-value UPI payments. The RBI gave its backing to the initiative as part of a broader push to improve reliability for everyday small-ticket transactions.

UPI Lite is currently available on several UPI-supported apps in India:

• BHIM (Bharat Interface for Money)

• PhonePe

• Google Pay

• Paytm

• Amazon Pay

• BHIM Axis Pay, BHIM AU 0101, and other bank-specific UPI apps

The UPI Lite registration process is built right into these apps — you don’t need a separate account or any new sign-up. If you’re already using a UPI payment app, you’re just one toggle away from activating it.

What Is the UPI Lite Transaction Limit and Wallet Cap?

Before you start using UPI Lite, it’s worth knowing exactly what the limits are — so you can plan your usage accordingly.

• Per transaction limit: You can make payments of up to ₹1,000 per transaction using UPI Lite. Anything above this must go through regular UPI.

• UPI Lite wallet limit (balance cap): The maximum balance you can hold in your UPI Lite wallet at any point is ₹5,000. If your wallet hits ₹5,000, you won’t be able to add more until you spend some of it.

• UPI Lite daily limit (top-up cap): You can add (top up) a maximum of ₹4,000 to your UPI Lite wallet in a single day. This is the UPI Lite daily limit for recharges, set by the RBI.

• UPI Lite transaction limit for offline mode: When using UPI Lite X (the offline version), the per-transaction limit remains ₹1,000, but the offline wallet balance cap is ₹2,000.

What Is UPI Lite X?

UPI Lite X is the offline extension of UPI Lite, launched by NPCI in September 2023. If UPI Lite makes online small-payments faster, UPI Lite X takes it a step further — letting you pay even without an active internet connection.

It uses NFC (Near Field Communication) technology for tap-to-pay transactions. You simply tap your NFC-enabled phone on a compatible POS terminal or device, and the payment is processed device-to-device without needing Wi-Fi or mobile data. This is what makes UPI offline payment a reality for everyday use.

Here’s what you need to know about UPI Lite X:

• Per transaction limit: ₹1,000 (same as standard UPI Lite)

• Offline wallet balance cap: ₹2,000

• Works via NFC, your phone and the merchant device must both support NFC

• Designed for areas with poor or no internet connectivity

• Currently available on select NFC-enabled Android devices

What Are the Features of UPI Lite?

UPI Lite isn’t just a stripped-down version of UPI — it’s a thoughtfully designed tool with specific features that make small-value cashless payments faster, simpler, and more reliable. Here’s a detailed look at each one:

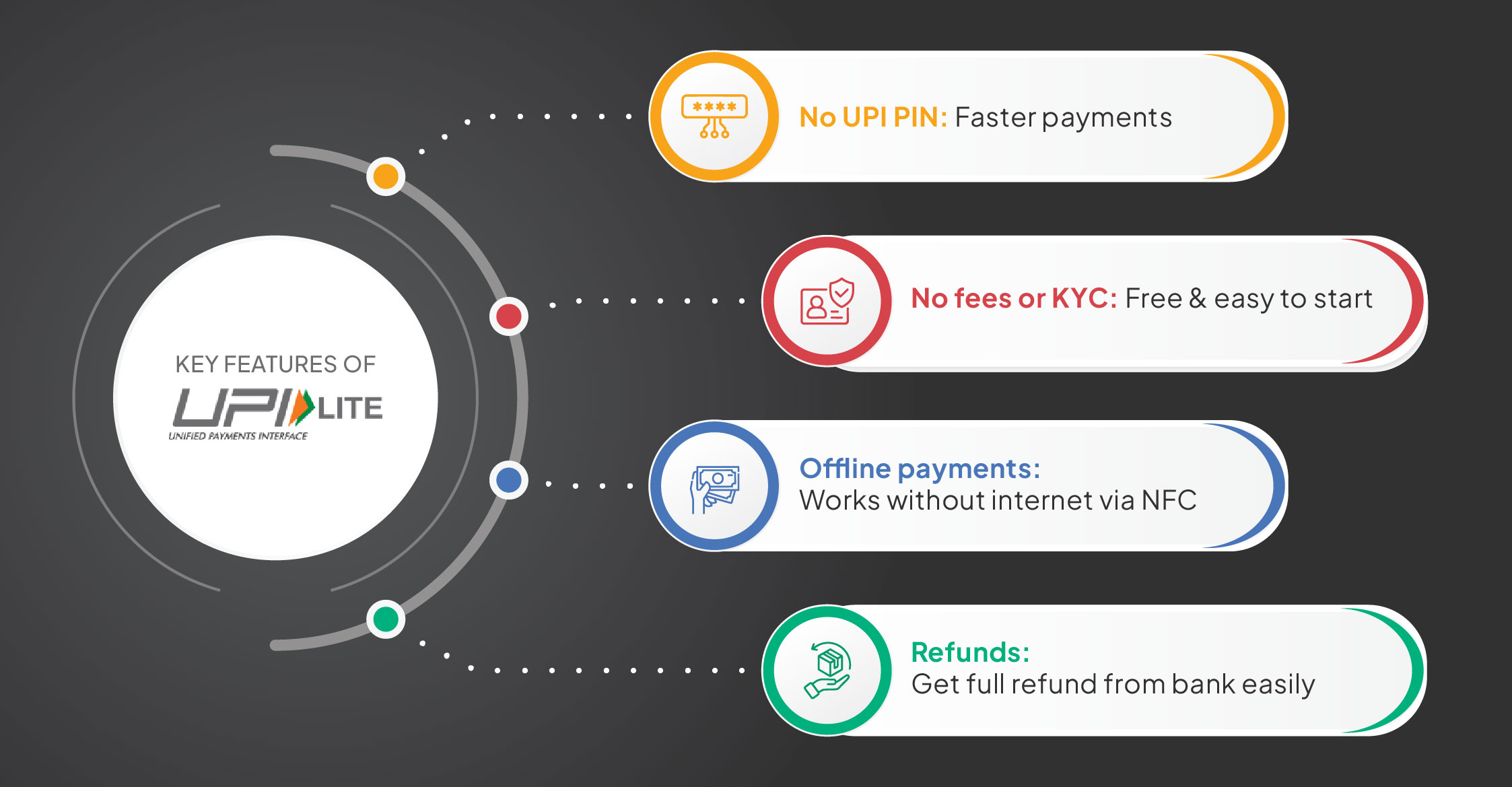

1. No UPI PIN Required

With UPI Lite, payments up to ₹1,000 go through without a PIN. You don’t have to type anything or wait for an OTP. The transaction happens in seconds, which is exactly what you want when you’re in a queue or making a quick purchase.

One important clarification though: the no-PIN rule applies only to payments made from your UPI Lite wallet. When you add money (top up) to your UPI Lite wallet from your bank account, you still need to enter your UPI PIN once. After that, all your payments from the wallet are PIN-free until the balance runs out.

2. Zero Fees and No KYC Required

UPI Lite has two user-friendly policies that make it accessible to practically everyone:

a) Zero transaction fees:

Using UPI Lite to make payments costs you absolutely nothing. There are no charges per transaction, no monthly fees, and no hidden deductions. Every rupee you load is every rupee you spend.

b) No KYC required:

You don’t need to complete any Know Your Customer (KYC) process to activate or use UPI Lite. No document uploads, no video verification, no waiting period. If you have a UPI app, you can enable UPI Lite right away.

Note: While UPI Lite itself doesn’t require KYC, your linked bank account must already be KYC-verified (as required by your bank). UPI Lite just doesn’t add an extra KYC layer on top of that.

3. Offline Payments via UPI Lite X

This is one of the most talked-about UPI Lite features — the ability to pay without internet. But here’s an important distinction: offline payment capability is specific to UPI Lite X, not standard UPI Lite.

Standard UPI Lite still needs an internet connection. UPI Lite X, on the other hand, uses NFC technology to enable tap-to-pay transactions between two NFC-enabled devices. The payment data is exchanged directly between your phone and the merchant’s terminal, no bank server, no internet required.

This makes UPI Lite offline payments ideal for:

• Rural areas or locations with poor network coverage

• Crowded places like metro stations or markets where network is congested

• Quick retail checkouts where speed matters

4. Refund Policy for UPI Lite

Note: UPI Lite does NOT support automatic refunds for failed merchant transactions. Unlike regular UPI, where a failed transaction typically triggers an automatic reversal, UPI Lite refunds for merchant failures need to be requested manually through your bank or UPI app support. Keep this in mind before using UPI Lite for merchant payments.

5. Transactions Recorded Only in App

Here’s something many users love about UPI Lite: its transactions don’t show up on your bank statement or passbook. Unlike regular UPI payments, which create a ledger entry every time, UPI Lite payments are recorded only within your UPI payment app’s transaction history.

Your bank statement will only reflect the top-up (when you add money to UPI Lite) — not every individual small payment you make from the wallet.

This is genuinely useful if:

• You want a cleaner, less cluttered bank statement

• You make dozens of small daily purchases and don’t want them all in your banking records

• You’re tracking personal spending through the app itself rather than your bank

How Does UPI Lite Work?

The process is simple and takes just a few minutes to set up. Here’s the step-by-step breakdown of how UPI Lite works — from first-time activation to making your first payment:

Step 1: Register and Activate UPI Lite

If you’re already an existing UPI user, you don’t need to do any of that. Just open your existing UPI app, go to settings or the wallet section, and look for the UPI Lite option. Tap to enable it

Step 2: Add Funds to Your UPI Lite Wallet

This top-up step does require your UPI PIN — just once per top-up. After you confirm it, the funds are transferred from your bank account to your UPI Lite wallet instantly.

Step 3: Make Payments Without UPI PIN

The payment happens instantly, and you’ll get a confirmation notification within the app. One thing to note: this confirmation appears in your UPI app, not as an SMS from your bank, because the transaction doesn’t go through the bank’s server.

What Are the Benefits of UPI Lite for Users and Merchants?

UPI Lite was designed to make small-value cashless payments better for everyone involved, whether you’re the buyer or the seller. Here’s how it benefits both sides:

Benefits of UPI Lite for Users

• Faster payments: No PIN means checkout is done in seconds — perfect for busy queues and quick purchases.

• Fewer transaction failures: Since payments are processed on-device rather than via bank servers, the failure rate drops significantly.

• Completely free to use: Zero fees, no minimum balance, no subscription — there’s genuinely no cost to using UPI Lite.

• No KYC hassle: Activate and start using immediately, without any document verification process.

• Works offline (via UPI Lite X): Pay even without internet using NFC-enabled devices, making UPI offline payment practical.

• Clean bank statements: Daily small transactions stay in your UPI app and don’t clutter your bank passbook.

• Versatile payment options: Pay via QR code, UPI ID, phone number, or bank account details — whichever suits you.

Benefits of UPI Lite for Merchants

• Faster checkout at point of sale: No customer fumbling with PIN means the queue moves faster and turnover improves.

• Lower payment failure rates: More transactions succeed, which means fewer awkward “payment failed” moments and no lost sales.

• Support for high-frequency small transactions: Ideal for businesses like food stalls, kirana stores, local shops, and transport services where small-value payments dominate.

• Offline payment acceptance (via UPI Lite X): Merchants in low-connectivity areas can still accept digital payments seamlessly.

• Improves digital payment adoption: The simplicity and speed of UPI Lite encourages more customers to pay digitally, boosting overall cashless payment volumes.

• Works with existing UPI payment gateway infrastructure: No extra setup needed — if you already accept UPI, you can accept UPI Lite payments too.

What Is the Difference Between UPI and UPI Lite?

| UPI does not support offline capability as it requires internet for all transactions | UPI Lite offers offline capability via UPI Lite X with NFC-enabled devices |

| Appears on bank statement and in app | Recorded only in the UPI app, not on bank statement |

UPI Lite vs UPI Lite X: What’s the Difference?

Both are part of the UPI Lite family, but they serve different use cases. Here’s how they compare:

| Feature | UPI Lite | UPI Lite X |

| Launch date | September 2022 | September 2023 |

| Connectivity required | Yes. It needs internet connection | No. It works fully offline via NFC |

| Technology used | Standard app-based processing | NFC (Near Field Communication) tap-to-pay |

| Per transaction limit | ₹1,000 | ₹1,000 |

| Wallet balance cap | ₹5,000 | ₹2,000 |

| Device requirement | Any smartphone with UPI app | NFC-enabled smartphone and compatible merchant terminal |

Start Simplifying Small Payments with UPI Lite

Whether you’re a user who’s tired of UPI failures at the neighborhood kirana store, or a merchant watching customers abandon payments because of a slow PIN entry screen, UPI Lite was built with you in mind.

For users, it means faster, PIN-free payments for everyday purchases, a cleaner bank statement, and the peace of mind that small transactions won’t fail. Activate UPI Lite on your preferred UPI payment app today. It takes under a minute and costs absolutely nothing.

For merchants, especially those running high-volume, small-ticket businesses like food stalls, local shops, auto services, or kirana stores, UPI Lite means a smoother checkout experience, more completed transactions, and customers who keep coming back because paying was effortless.

And if you’re a business owner looking to offer your customers a reliable, full-featured payment experience including UPI, UPI Lite, cards, wallets, and more, a trusted UPI payment gateway partner like PayU can make all the difference. PayU supports the complete spectrum of UPI payments and is built for businesses that want fewer payment failures and faster growth.

FAQs

What is UPI Lite?

UPI Lite is an on-device wallet within your UPI app, backed by NPCI and the RBI, that lets you make small-value payments up to ₹1,000 without entering a UPI PIN — making transactions faster and more reliable.

What is the transaction limit for UPI Lite?

The UPI Lite transaction limit is ₹1,000 per payment. You can top up your wallet by up to ₹4,000 per day, and the maximum wallet balance you can hold is ₹5,000.

Is UPI Lite safe to use for payments?

Yes. UPI Lite is built on NPCI’s secure UPI infrastructure. While it skips the PIN for small payments, the wallet is tied to your verified bank account and protected by your phone’s app-level security.

Which banks support UPI Lite in India?

Most major banks in India support UPI Lite, including SBI, HDFC, ICICI, Axis, Kotak, and many others. You can check your specific bank’s UPI Lite eligibility in your UPI app when activating the feature.

Can I use UPI Lite without an internet connection?

Standard UPI Lite requires an internet connection. For true offline payments, you need UPI Lite X, which uses NFC technology to process transactions without internet on compatible devices and merchant terminals.

What happens if a UPI Lite payment fails?

Unlike regular UPI, UPI Lite does not support automatic refunds for failed merchant transactions. You’ll need to manually contact your bank or raise a dispute through the UPI app’s support section to get a refund.

Can I transfer my UPI Lite balance back to my bank account?

Yes. You can transfer the remaining UPI Lite balance back to your linked bank account at any time by selecting the “Disable” or “Transfer Back” option in the UPI Lite section of your app. The amount is credited to your bank account instantly.