AI-Powered Summary

- Payment tokenization replaces sensitive card information with a random, unique token to enhance security during transactions.

- The token is meaningless on its own, cannot be reverse-engineered, and only works within the specific authorized payment context.

- Tokenization reduces fraud risks, builds customer trust, and simplifies compliance with regulations like India's RBI guidelines.

- The process involves generating a token, securely storing card data in a token vault, and using the token throughout the payment system.

- Tokenization supports faster checkouts, secure recurring payments, and safer in-store and mobile transactions.

- Businesses benefit from reduced liability, lower compliance costs, and improved customer experience through tokenization.

Every time a customer pays with their card online, sensitive data such as the card number, expiry date, CVV travels through multiple systems. And every system it touches is a potential risk. Data breaches don’t just cost money. They damage trust, invite regulatory penalties, and can take years to recover from.

That’s exactly why payment tokenization exists. It’s one of the most effective ways to protect card data without disrupting the payment experience for you or your customers.

In this guide, you’ll learn what payment tokenization actually means, how it works step by step, the different token formats used in payments, the business benefits it brings, and what India’s RBI guidelines say about it. Whether you’re setting up a payment gateway for the first time or looking to tighten your existing security, this is a good place to start.

Table of Contents

What Is Payment Tokenization?

Payment tokenization is a security process that swaps out sensitive card information, like your 16-digit card number with a random, meaningless string of characters called a token. This token acts as a stand-in for the real card data during transactions.

However, the token has no real value on its own as it doesn’t contain any actual card information. So even if someone intercepts it, there’s nothing useful to steal.

What is payment tokenization in practice? It means your card number never gets stored by the merchant. Instead, a secure system holds the original data in a locked vault, and only the token circulates through payment systems. The merchant, their servers, and even their payment gateway never see your real card number, just the token.

What Is a Token in Payments?

A token is simply a random substitute for your card number. It could look like this: 25c92e17-80f6-415f-9d65-7395a32u0223. It follows no pattern, carries no account information, and can’t be reverse-engineered.

Let’s say your card number is 4512 8763 9021 4455. After tokenization in payment, the system generates a completely different string to represent it. Something like 7b29dc34-k8m1-220f-ab43-99182l760011. That string is what gets stored and transmitted. It’s unique to the combination of your card, the merchant, and the device being used.

However, the token only works within the specific, authorised payment context it was created for. If someone steals a token and tries to use it elsewhere, it won’t work. There’s no account attached to it, no card number, no path back to your real data, unless you’re the authorised system with the right access.

This is what makes card data protection so much stronger with tokenization. Unlike encryption, where the original data can be decrypted with the right key, tokenization doesn’t use a reversible mathematical relationship between the token and the original number. It’s irreversible by design.

Why Tokenization Is Important for Merchants?

If you’re a merchant, whether you run an online store, a subscription service, or a physical shop, tokenization directly impacts your risk and your customer experience.

Here’s why it matters for your business:

• It reduces fraud because even if your systems are compromised, the attacker only gets tokens, not real card numbers.

• It builds customer trust. Shoppers are more likely to save their card details on a platform they trust, which leads to faster checkouts and higher repeat purchases.

• It supports saved cards for returning customers, making it easier to offer one-click payments.

• It helps you comply with RBI tokenization guidelines, which as of October 2022, prohibit merchants from storing actual card data. Merchant tokenization is now the compliant path forward.

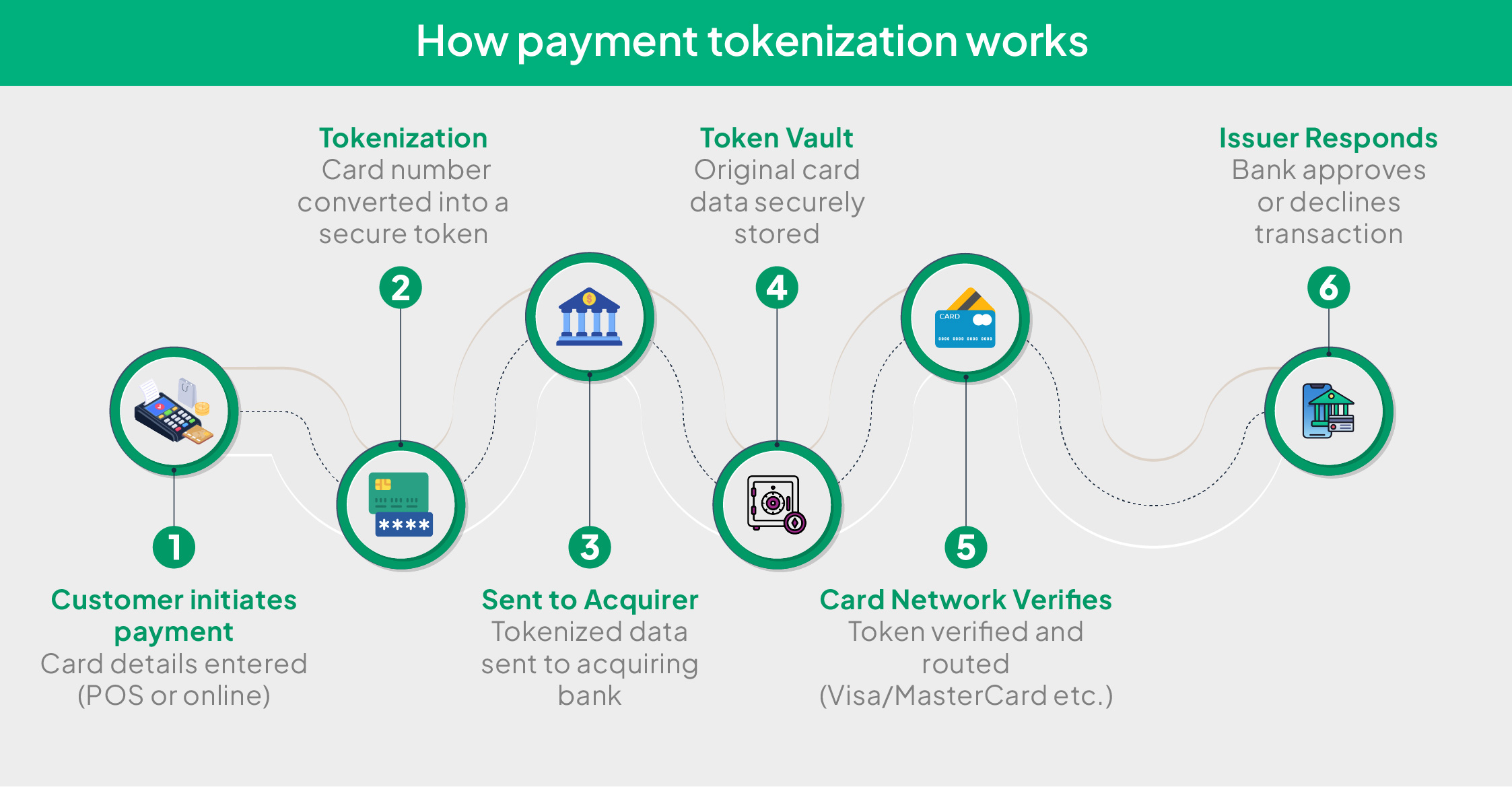

How Payment Tokenization Works?

Tokenization of debit card payments and other payment modes transforms sensitive card data into a non-sensitive equivalent that can be stored and safely transmitted without exposing the actual payment-related data to potential threats or fraud. In the context of payment processing, the working of Tokenization is as follows.

Step 1: Customer Enters Card Details

The process kicks off when a customer enters their card details, either on your website’s checkout page or by tapping or swiping at a POS (point of sale) terminal in your store.

That card information is collected for one purpose only: to initiate tokenization. Your system never stores the card number, expiry date, or CVV. The data is passed directly and securely to the tokenization service and from that point, the actual card details are no longer part of your environment.

Step 2: The Token Is Generated

The tokenization service takes the card data and converts it into a unique token, a random string that represents the card without exposing it.

Depending on the system and card network rules, this token may be reversible (meaning the original data can be retrieved by the authorised vault) or non-reversible (where the token simply maps to the card data via a lookup table, with no mathematical path back). Most modern card tokenization systems use the latter for stronger security.

The generated token is then sent back to your checkout or POS system to replace the card number in your records.

Step 3: Tokenized Request Is Sent for Processing

The tokenized transaction details are forwarded to the acquirer which is the bank or financial institution that processes payments on your behalf.

The transaction moves through the entire payment infrastructure using the token, not the real card number. This means every layer of the payment system, including third-party processors and intermediaries, handles only a meaningless token. Your customer’s real card data stays out of the picture.

Step 4: Card Data Is Stored Securely in the Token Vault

Behind the scenes, the original card data isn’t just floating around but instead it’s stored in a highly secure environment called a token vault. Think of the token vault as a locked safe that maps each token back to the real card details.

Only authorised systems, like the card network or issuing bank can access the vault to retrieve or ‘detokenize’ the data when it’s needed for verification. Merchants, payment gateways, and third-party services never get access to this vault. This separation is exactly what makes PCI DSS tokenization standards achievable for businesses.

Step 5: The Card Network Verifies the Token

The acquirer sends the tokenized request to the card network. It could be Visa, Mastercard, RuPay, or another network. The card network validates the token, confirms it’s legitimate and correctly formatted, and routes the transaction to the card issuer. The real card number never needs to appear in this step, the token is accepted across all authorised payment rails.

Step 6: Issuer Approves or Declines the Payment

Finally, the card-issuing bank receives the request and makes the call. It checks the customer’s account balance, runs fraud detection checks, and either approves or declines the transaction. An approval or decline message then flows back through the chain to the card network, acquirer, and finally to your checkout.

From the customer’s perspective, this whole process takes just a few seconds. But internally, their card data was protected at every step and your systems never held the sensitive information at all.

What Are the Types of Payment Tokenization?

Not all tokens look the same. The types of tokenization differ based on how the token is formatted relative to the original card number. Here are the three main formats you’ll come across:

Non-format preserving tokens

In non-format-preserving tokens, the tokens take an entirely different format, and they do not resemble the original credit card number. The tokens typically include a random set of alphanumeric characters.

For example, if your card number is 1468 2356 7869 8901

The non-format preserving token could be 24c82e19-79c4-104x-0l35-3798s45y1882

Format-preserving tokens

In format-preserving tokens, as the name itself suggests, the tokens maintain the same format as the original card information. However, the values of the are changed randomly.

For example, if your card number is 1468 2356 7869 8901

The format-preserving token could be 7690 2498 1121 2500

Partial Replacement Tokens

A partial replacement token is a type of format-preserving token in which some of the values are left unchanged. This is also commonly referred to as selective masking, and it is a very common practice for payment tokens. It is often used for display and customer service use cases for example, showing a customer their saved card on a checkout page, or helping a support agent identify a card without seeing the full number.

For example, if your card number is 1468 2356 7869 8901

The partial preserving token could be 1468 2480 4892 8901 or 1468 AUH# BID& 8901

What Are the Benefits of Payment Tokenization for Businesses?

Now that you know how payment Tokenization worksand its different formats, let us explore the importance of payment Tokenization for various types of businesses.

Payment Tokenization offers a wide range of benefits for different types of businesses that accept payments via debit or credit card and other digital payment modes

Improved Security

Whenever a breach happens, tokenization limits the damage. Because your systems hold tokens instead of real card numbers, attackers can’t extract usable card data even if they get in. This protection applies to both online transactions and in-store payments, dramatically cutting fraud risk across the board.

Legal Compliance and PCI DSS Alignment

Storing card data means taking on a heavy compliance burden. PCI DSS tokenization requirements demand that any system holding cardholder data meets strict security standards which takes time, money, and ongoing audits. By replacing card data with tokens, you reduce the scope of your PCI DSS environment significantly. Fewer systems in scope means simpler, cheaper compliance. And with India’s RBI tokenization guidelines prohibiting merchants from storing raw card data since October 2022, tokenization isn’t just good practice, it’s the compliant way to operate.

Faster, Safer Checkout Experience

Nobody likes re-entering their card details every time they shop. With secure online payments powered by tokenization, returning customers can check out with a single tap, their saved card token is retrieved, and the transaction goes through without them having to type anything. This reduces friction at checkout, cuts cart abandonment, and keeps repeat customers coming back.

Better Subscription and Account Management

If you are running a subscription service, tokenization makes life a lot easier. When a customer upgrades, downgrades, or cancels their plan, you don’t need to re-collect their card details, the token handles it. The same token can be used to process recurring payments, manage plan changes, and update billing information, all without ever touching the actual card data. It keeps the process smooth for your customers and secure for your business.

Secure POS (Point of Sale) Payments

In-store payments carry risk too. When card data sits inside a POS system, it becomes a target. Tokenization removes that risk by ensuring sensitive data is never stored within the POS terminal itself. The moment a card is tapped or swiped, the data is tokenized before it touches any local storage, protecting both you and your customers at the point of purchase.

Secure Mobile and Wallet Payments

Digital wallets, contactless cards, and mobile payment apps all rely on tokenization to function safely. When a customer pays with Google Pay, Apple Pay, or any NFC-enabled card, a token specific to that device and transaction is used, never the actual card number. This is what makes tap-to-pay and mobile payments secure by default. Tokenization is the invisible security layer that powers modern, frictionless payment experiences.

Reduced Business Liability

The less sensitive card data you hold, the less you’re on the hook for if something goes wrong. Card data protection through tokenization directly reduces your exposure to breach-related penalties, regulatory fines, and costly chargebacks. It also protects your brand, a data breach can shake customer confidence for years, and limiting your stored card data is one of the best ways to prevent that from happening.

Cost Control and Lower Risk Exposure

Managing your own card data storage is expensive. You need dedicated security infrastructure, regular audits, encryption tools, and trained staff to maintain compliance. Tokenization shifts that responsibility to a specialised vault provider, which means lower operational overhead for you. And since the risk of a costly breach drops significantly, so does your potential exposure to legal fees, compensation costs, and reputational damage.

RBI Guidelines for Tokenization in India

The RBI has allowed the Tokenization of debit card, credit card, and prepaid card transactions in India, primarily with the aim of promoting digital payments and protecting customer data. In that regard, the RBI has also issued certain guidelines for Tokenization services, including:

1. Tokenization is not mandatory, but a business organization can implement it voluntarily in their payment process, requiring explicit consent through AFA (Additional Factor of Authentication).

2. Card companies have the authority to decline tokenized payment requests for security reasons.

3. As of October 1, 2022, all online merchants and business owners who have implemented Tokenization in their payment processes are prohibited from saving customers’ card details.

Conclusion

Payment tokenization is one of those things that works quietly in the background, but the impact it has on security, compliance, and customer experience is anything but small. It protects real card data from exposure, keeps you on the right side of RBI and PCI DSS requirements, and makes checkout faster and easier for your customers. Whether you’re running an e-commerce store, a subscription business, or a physical retail outlet, tokenization is the kind of infrastructure that pays for itself.

If you’re a merchant looking to offer secure, seamless card payments with full tokenization support built in, PayU has you covered. PayU’s payment gateway is RBI-compliant and supports card tokenization, so your customers get a smooth, secure checkout experience, and you get peace of mind.

FAQs

Payment tokenization is a security process that replaces sensitive card information like your 16-digit card number with a random, unique string of characters called a token. The token is used in place of real card data during transactions, so the actual card details never get stored or exposed.

Is tokenization safe for online card payments?

Yes, it’s one of the safest methods available. Tokens carry no real card data, can’t be reverse-engineered, and only work within the specific, authorised system they were created for.

What is a token vault in payment tokenization?

A token vault is a secure, centralised system that stores the original card data and maps it to the corresponding token. Only authorised systems like the card issuer can access it for verification purposes.

How does payment tokenization work?

When a customer enters their card details, the tokenization service replaces the card number with a unique token. That token is used throughout the transaction process, through the acquirer, card network, and issuer — while the real card data stays locked in a secure vault.

What are the types of payment tokens?

There are three main types: non-format preserving tokens (completely different from the card number), format-preserving tokens (same 16-digit structure, different values), and partial replacement tokens (only some digits are changed, used for display purposes).

Is tokenization mandatory in India?

Tokenization itself is not mandatory, but since October 2022, merchants are prohibited from storing actual card data, which effectively makes tokenization the only way to offer saved cards to customers.

What are the RBI tokenization guidelines?

The RBI has made tokenization voluntary but banned merchants from storing raw card data from October 1, 2022. Customers must give explicit consent (via AFA) to tokenize their cards, and they can set limits or suspend tokens at any time.

Can tokenization be used for recurring payments?

Absolutely. Tokens can be reused for subscriptions, recurring billing, and plan changes making them ideal for businesses that need to charge customers on a regular basis without handling card data directly.

Does tokenization work for POS payments too?

Yes. Tokenization works for in-store card transactions as well, preventing sensitive card data from ever being stored in POS machines or local systems.

How can merchants benefit from payment tokenization?

Merchants benefit from reduced fraud risk, simpler PCI DSS compliance, faster checkout for returning customers, lower breach liability, and the ability to support saved cards, recurring billing, and mobile/wallet payments, all while staying compliant with RBI rules.