AI-Powered Summary

- Payment processing is a secure system that transfers money from a customer’s account to a merchant’s account during a transaction, involving multiple players like payment gateways, processors, and banks.

- A payment gateway encrypts and collects payment details, while a payment processor authorises and moves the funds, with many providers offering both as a combined solution.

- Key benefits of payment processing include faster checkouts, enhanced security, reduced manual tasks, support for multiple payment methods, and predictable cash flow.

- The payment process involves steps like capturing payment details, encryption, bank verification, authorisation, and final settlement to the merchant’s account.

- Businesses should choose payment processing solutions based on factors like PCI DSS compliance, customer support, flexibility, supported payment methods, and transparent fees.

Payment processing is the end-to-end system that securely moves money from your customer’s account to yours every time a purchase is made.

In the modern digital business landscape, it wouldn’t be wrong to say that payment processing is the backbone of all financial transactions. And for anyone who owns a business, whether it’s a small start-up or a large enterprise across various sectors, it is paramount that they understand the nuances of payment processing.

It will help them establish an efficient payment processing systemin their business, facilitate safe and secure transfer of funds, and offer a seamless payment solution to their customers. In this blog, we’ll walk you through:

• What payment processing actually means

• How it’s different from a payment gateway

• The key players behind every transaction

• A step-by-step breakdown of how it works

• The real benefits for your business

• What to look for when choosing a payment processing solution

What Is Payment Processing?

At its core, payment processing is the secure flow of money from a customer to a merchant. It’s everything that happens in those few seconds between a customer clicking “Pay Now” and you receiving confirmation that the payment went through.

This flow takes into account several factors that work together behind the scenes. Right from payment gateways that capture and encrypt transaction data to payment processors that route that data to the right banks to issuing banks that verify the customer’s funds, and card networks like Visa, Mastercard, or RuPay that connect it all.

As a result, a seamless, secure transaction takes just a few seconds, even though a lot is happening in the background.

What Is the Difference Between Payment Processing & Payment Gateway?

This is one of the most common points of confusion for businesses setting up online payments. Here’s the simplest way to think about it:

A payment gateway is the secure front-end interface. It’s what collects your customer’s payment details at checkout, encrypts them, and passes them on safely. Think of it as the locked door that protects sensitive card data.

A payment processor, on the other hand, is what actually moves the money. It communicates with the customer’s bank and the card network, handles payment authorisation, and determines whether a transaction is approved or declined.

So, the key difference between payment gateway and processor is this: the gateway collects and secures the data, while the processor acts on it.

In practice, many providers offer both as part of one payment processing solution, so you don’t always need to set them up separately.

Why Payment Processing Matters for Businesses?

If you’re running any kind of business that accepts digital payments, whether online, in-store, or both, having a reliable payment processing system isn’t optional. Here’s why it matters:

• Faster checkout experience: Customers can pay in seconds with the method they prefer, be it cards, UPI, wallets, or net banking.

• Fewer manual tasks: Payments get recorded and reconciled automatically, saving your team hours of work.

• Better security: Built-in encryption and fraud detection keep both you and your customers protected.

• More payment options: The more ways customers can pay, the fewer sales you lose at checkout.

• Smoother cash flow: Payment settlement happens on a predictable schedule, so you always know when funds are hitting your account

Key Players in Payment Processing

Although on the surface it may seem that payment processing is a transaction occurring between a customer and a business or enterprise, there are many other parties or players involved in the transaction who play a crucial role in completing the payment. These players are:

Customer

The customer is the one initiating the payment. At checkout, they choose how they want to pay either by entering card details, scanning a UPI QR code, selecting a saved wallet, or using net banking. Once they authorise the transaction, the payment process begins.

Merchant

That’s you. The merchant is the business collecting the payment. You initiate the sale, provide a checkout experience for your customer, and receive the funds once the transaction is authorised and the payment settlement is complete.

Payment Gateway

The payment gateway is the secure interface that sits between your customer and the payment system. It captures the payment details, encrypts them so they can’t be intercepted, and forwards the transaction data to the processor for authorisation.

Payment Processor

The processor is the engine running in the background. It receives the encrypted data from the gateway, routes it to the relevant card network and banks, and relays the final decision back. If a payment is approved or declined, it’s the processor communicating that outcome.

Issuing Bank

This is the customer’s bank — the institution that issued their card or manages their account. It’s responsible for checking whether the customer has sufficient funds, whether the card is valid, and whether any fraud signals are raised. Based on all of this, it either authorises or declines the transaction.

Acquiring Bank

The acquiring bank is your bank as a merchant. It receives the incoming funds from the issuing bank, processes the payment settlement, and credits the net amount to your merchant account, after deducting any applicable fees.

Card network – It is the global network that connects issuing banks with acquiring banks. The most popular card networks in India are MasterCard, Visa, and American Express

How Payment Processing Works?

Right from the moment a customer taps “Pay” to the time money lands in your account, a lot of events take place in the background. Let’s take a step-by-step look at how payment processing works.

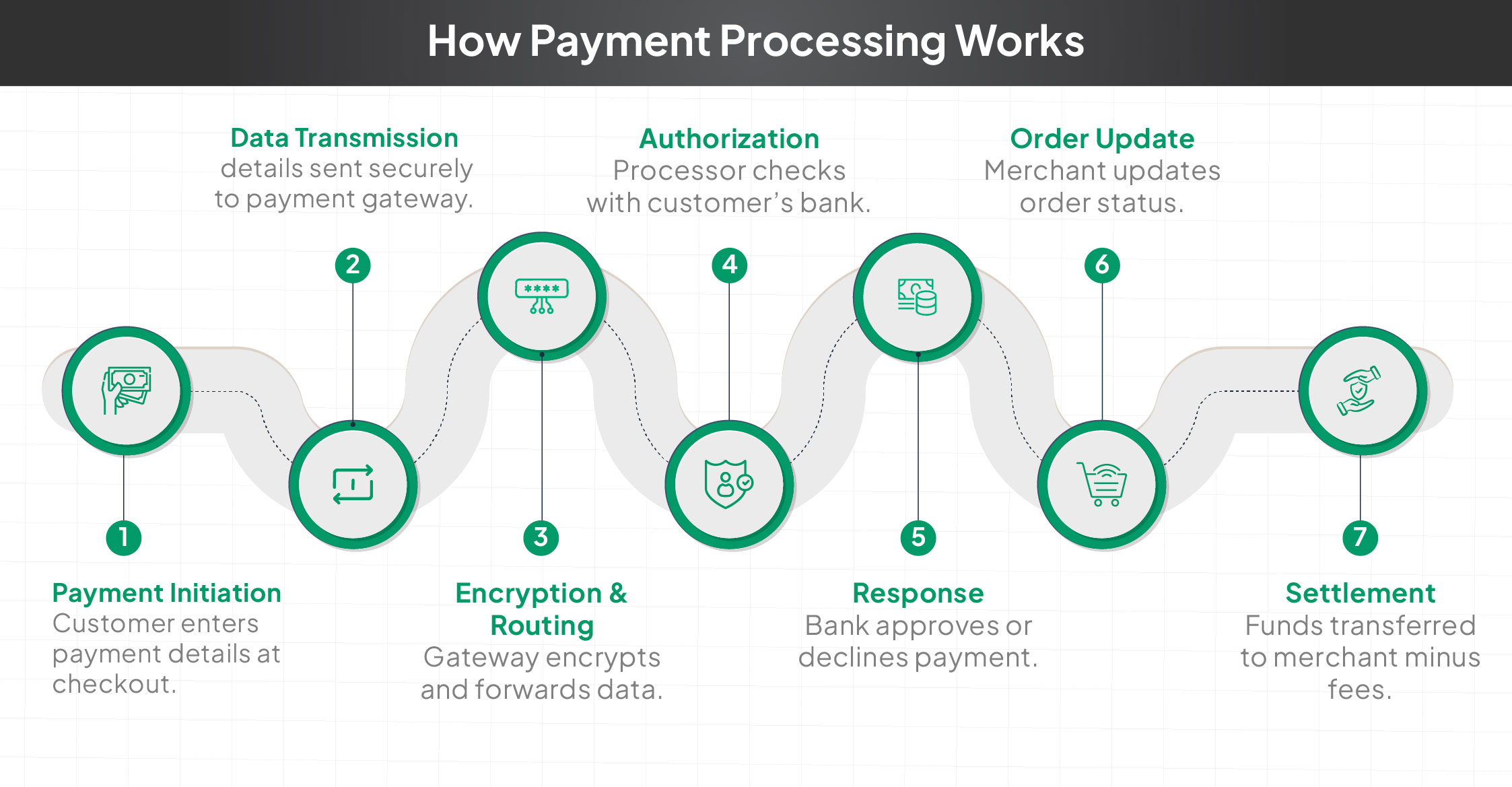

Step 1: Customer Starts Checkout

It all starts when a customer selects a product or service and heads to checkout. At this point, they’ll choose how they want to pay, by credit or debit card, UPI, a digital wallet, or net banking. Once they’ve made their choice and entered their details, the transaction is ready to begin.

Step 2: Payment Details Are Captured Securely

As soon as the customer submits their payment, your website or app captures that information and passes it to the payment gateway integrated into your platform. The customer’s sensitive card or account details never sit exposed. They’re handled through secure, encrypted channels from the very first moment.

Step 3: Payment Gateway Encrypts and Processes the Request

The payment gateway receives the data and immediately encrypts it by scrambling the information so that even if it’s intercepted, it’s unreadable. Once encrypted, the gateway forwards the transaction to the correct payment processor or card network to continue the authorisation process.

Step 4: Bank Verifies and Authorises the Payment

The payment processor sends the transaction to the customer’s issuing bank. The bank then runs a quick series of checks like, does the account have enough funds? Is the card valid and active? Are there any fraud signals or unusual patterns? Based on these checks, the bank sends back either an approval or a decline. This is what payment authorisation looks like in practice.

Step 5: Processor Sends Approval or Decline

Once the bank responds, the processor picks up that message and relays it back to the payment gateway. If it’s an approval, the checkout flow continues. If it’s a decline, the customer is notified and prompted to try a different payment method, all within seconds.

Step 6: Merchant Order Status Is Updated

Your system receives the result and updates the order accordingly by marking it as paid or failed. For successful payments, this confirmation triggers the next stage: settlement. For failed payments, no money moves and the order remains pending or is cancelled.

Step 7: Funds Are Settled to the Merchant

Payment settlement is the final step and it’s when the money actually hits your account. The acquiring bank transfers the approved funds to your merchant account, usually on a daily or weekly cycle depending on your payment provider. Before the funds arrive, applicable processing fees are deducted. Once settled, the transaction is complete.

Benefits of a Payment Processing System for Businesses

A solid payment processing setup does more than just accept money. Here’s what it can actually do for your business.

Better Customer Experience

When customers have more ways to pay and fewer steps to complete a purchase, they’re more likely to follow through. A smooth checkout experience — one that works on mobile, accepts multiple payment methods, and doesn’t throw up unnecessary errors — reduces friction and keeps customers coming back. Fewer payment failures also means fewer frustrating moments right at the final step.

Higher Sales and Conversion Rates

A slow or limited checkout is one of the biggest reasons customers drop off before completing a purchase. When your payment processing for businesses supports a wide range of payment methods and moves quickly, it reduces drop-offs and encourages impulse purchases. Every improvement in checkout speed and flexibility can have a direct impact on your conversion rate.

Lower Operational Costs

Manual payment reconciliation is time-consuming and prone to errors. A modern payment processing system automates much of this, matching payments to orders, updating records, and flagging discrepancies without needing someone to do it by hand. That means less effort from your finance team, fewer mistakes, and lower overall operational costs.

Seamless Integration with Existing Systems

Most modern payment processing solutions are built to work with the tools you already use. Whether you’re on WooCommerce, Shopify, a custom-built platform, or a mobile app, you’ll find plugins, APIs, and low-code integration options that make setup straightforward. You don’t need a dedicated engineering team to go live, in many cases, you can be up and running in a matter of hours.

Stronger Security and Fraud Protection

Online transaction security is non-negotiable for any business accepting digital payments. Good payment processing systems come with end-to-end encryption, tokenisation, and real-time fraud detection built in. This means suspicious transactions are flagged faster, customer data is protected throughout the process, and your business is far less exposed to payment fraud and data breaches.

Faster Cash Flow and Settlement Visibility

One often overlooked benefit is what faster payment settlement does for your working capital. When funds arrive in your account on a predictable schedule, you can plan purchases, manage inventory, and cover expenses more confidently. Most modern payment dashboards also give you real-time visibility into pending and completed payments, so you always know exactly where your money is.

How to Choose the Right Payment Processing Solution?

Businesses looking to integrate a payment processing system into their platform to facilitate easy, quick and secure payment processing must be careful and choose the right system to suit their specific needs. Some of the important factors that they must take into account are:

PCI DSS Compliance

PCI DSS (Payment Card Industry Data Security Standard) compliance is the baseline requirement for any payment system handling cardholder data. When your payment processing security meets this standard, it means your system follows strict protocols for storing, processing, and transmitting card information. Non-compliance isn’t just a technical issue. It can expose your business to data breaches, legal penalties, and serious reputational damage. Always verify that your provider is PCI DSS certified before going live.

Reliable Customer Support

Payment issues don’t always happen at convenient times. If a customer hits an error at checkout, or you’re dealing with a dispute during a sale peak, you need support you can reach quickly. Look for a provider that offers responsive, multi-channel support — especially if you’re running live transactions around the clock. Fast issue resolution during checkout, integration problems, or settlement queries can make a real difference to your operations.

Customisation and Flexibility

Your business has specific needs, and your payment system should accommodate them. A good payment processing solution will let you customise your checkout branding to match your identity, configure which payment methods you offer, and build workflows that fit your business model. Whether you need subscription billing, split payments, or a branded payment page, flexibility here matters a lot as you scale.

Supported Payment Methods

In India, the range of payment methods your processor supports can be the deciding factor. You want a provider that covers UPI, credit and debit cards, net banking, digital wallets, EMI options, and payment links. The broader the support, the fewer customers you lose at checkout due to their preferred method not being available.

Transparency in fees

A transparent fee structure is necessary. Businesses must understand that the processing rates for different types of cards and details regarding various fees, like monthly statement, batch fees, etc. Payment processing solutions and payment links play an important role in achieving these criteria.

Conclusion

Payment processing is the cornerstone of modern businesses. It is an intricate process that ensures the swift exchange of funds between customers and businesses in a secure way. Businesses can leverage the various benefits of a well-structured and robust payment processing system. It helps reduce the administrative cost, boosts sales, provides a better shopping experience to the customers, facilitates payments through different modes as per the customers’ preferences and fosters customer loyalty.

A payment processing system can also help businesses use automation for handling tasks like authorising the payments, eliminating the need for having a dedicated resource and allocating them for other critical business operations. Finally, a payment processing system can help keep track of the everyday transactions, analyse them and gain valuable insights on the spending trend, the customer preferences and enhance the offering for better outcomes.

FAQs

Payment processing is the secure, end-to-end system that moves money from a customer’s account to a merchant’s account when a digital transaction is made. It covers everything from capturing payment details at checkout to final payment settlement.

What is the difference between a payment gateway and a payment processor?

A payment gateway collects and encrypts payment data at checkout. A payment processor takes that data and handles the actual authorisation by communicating with the relevant banks and card networks. Understanding this difference between payment gateway and processor helps you pick the right setup for your business.

Who are the key players in payment processing?

The main parties involved are the customer, the merchant, the payment gateway, the payment processor, the issuing bank (the customer’s bank), and the acquiring bank (the merchant’s bank). Card networks like Visa, Mastercard, and RuPay also play a key role in connecting these parties.

How does payment processing work?

The customer enters their payment details at checkout, the gateway encrypts and forwards the data to the processor, the processor requests authorisation from the issuing bank, and the bank approves or declines. The result is passed back through the chain, and if approved, the merchant settlement follows on the agreed schedule.

Why is payment processing important for businesses?

It enables businesses to accept digital payments securely, reduces manual admin work, supports multiple payment methods, and ensures funds settle into your account reliably. Without it, accepting online or card-based payments simply isn’t possible.

How long does payment settlement take?

Settlement timelines typically range from T+1 to T+3 business days, depending on your payment provider and the payment method used. Some providers offer faster or same-day settlement options for eligible merchants.

What should businesses look for in a payment processing solution?

Look for PCI DSS compliance, responsive customer support, support for multiple payment methods (UPI, cards, wallets, EMI), flexible integration options, and transparent fee structures. Secure payment processing and settlement visibility are also important.

How can PayU help with payment processing?

PayU offers a comprehensive payment processing system that supports all major Indian payment methods, including UPI, cards, wallets, and net banking. With easy API integration, built-in fraud detection, and real-time settlement tracking, PayU helps businesses of all sizes accept payments smoothly and securely.

Can payment processing help increase revenue?

Yes. Offering more payment options, reducing checkout friction, and minimising payment failures all contribute to higher conversion rates. The benefits of payment processing extend beyond just accepting money — they directly impact how many sales you complete and how smoothly your business runs.