The Indian taxation system charges MSMEs direct and indirect taxes. Direct tax is a tax on income, whereas indirect tax is passed on to the end consumer.

-

- Last updated: July 11, 2022

- 4 minute read

AI-Powered Summary

- The Union Budget now focuses more on direct taxes, with indirect taxes like GST being addressed separately.

- Direct taxes are paid directly by companies on their income, while indirect taxes are levied on the sale of goods and services and passed on to consumers.

- Direct taxes include corporate tax, capital gains tax, and income from other sources, while indirect taxes include GST, customs duty, and VAT on specific items like liquor and tobacco.

- GST has replaced multiple indirect taxes, operates under a dual structure, and requires state-wise registration with varying tax slabs.

- India's tax regime remains complex, causing challenges for MSMEs, highlighting the need for efficient IT solutions to manage tax liabilities.

The Union Budget has traditionally been about indirect taxes and how each year’s goods and services would become costlier because of the new rates of tariffs imposed by the government.

But with GST coming into the scene, the Union Budget only spoke of import duty and no other indirect taxes. So today, the budget presentation focuses more on direct taxes and their implication on corporations and individuals.

This article discusses direct and indirect taxes for corporations in India.

| 1. | What are Direct and Indirect Taxes? |

| 2. | Difference Between Direct & Indirect Tax |

| 3. | Types of Direct & Indirect Tax |

What are Direct and Indirect Taxes?

Even though payable by the organization, direct and indirect taxes are vastly different from each other.

Taxes are mainly classified into two categories – direct and indirect.

As the name suggests, direct taxes are paid by the companies to the government directly. Even, the taxes can’t be passed on to other entities. Income tax is the direct tax on the earnings of a company. These are not passable and will be borne by the entity liable to pay. In most cases, domestic companies are responsible for paying a flat 30% along with a surcharge (if applicable) on their earnings. In comparison, foreign companies have to bear a more stringent tax rate of 40% on their income along with a surcharge (If any).

On the other hand, indirect taxes are charged on the sale of any product or service. These won’t come into the picture if you do not sell anything deemed taxable by the government. Previously, VAT and Service Tax were charged on the sale of goods and services, respectively. With the inclusion of GST, there is a single tax for a majority of offerings.

Difference Between Direct & Indirect Tax

While the responsibility of paying indirect and direct taxes lies with the corporate house, there are some stark differences between these two:

- Even though direct and indirect taxes are levied on all eligible entities, the end consumer bears indirect tax, whereas each entity is eligible to pay its share of direct taxes.

- Direct tax is a single-stage tax applicable on certain transactions or income of the company. In contrast, indirect tax is a multi-stage tax levied on each stage of production and distribution of the offering.

- Direct taxes are non-transferable, whereas indirect taxes are transferable. Therefore, the entity that pays indirect tax for buying an offering can claim it as input tax in most cases.

- A corporate house can generate income tax benefits by investing in tax saving instruments or fulfilling specific criteria established by the government. But there is no way to evade indirect taxes or reduce its liability.

Types of Direct & Indirect Tax

There are a plethora of direct and indirect taxes applicable to companies operating in India.

Types of Direct Taxes

Corporate direct tax is taxable on income by the company in India. It includes the following:

- Profits and gains from business and profession

- Capital gains

- Earnings from house property

- Earnings from other sources

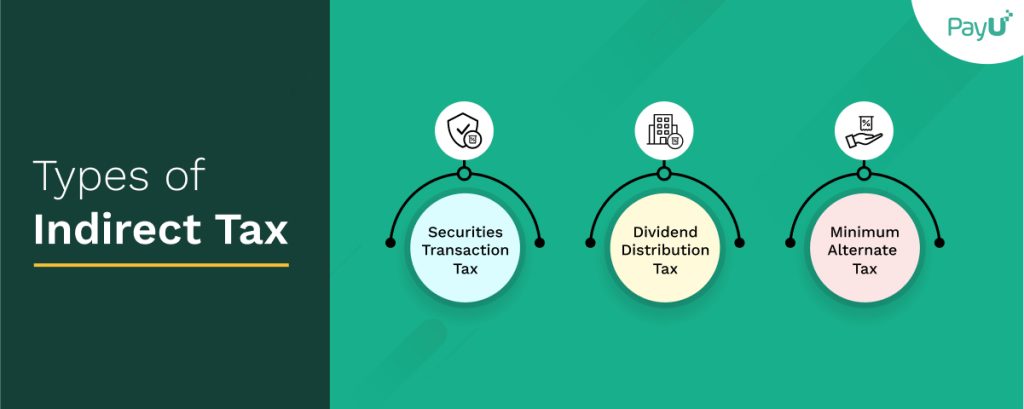

Types of Indirect Taxes

In addition, companies are also liable to pay the following indirect taxes (if applicable):

- Securities Transaction Tax (STT) on the sale of securities listed on the stock exchanges in India. It includes shares, stocks, scrips, derivatives, Equity Linked Savings Scheme, and more.

- Dividend Distribution Tax (DDT) on payment of dividends to shareholders

- Minimum Alternate Tax (MAT), if the entity is a zero tax company opting to pay taxes under the MAT structure.

As for indirect taxes, GST (Goods and Services Tax) is the major contributor for entities. It subsumed a host of indirect taxes that prevailed before. India follows a dual structure where the center and the states or union territories can share the inflow pre-decidedly.

GST is levied on a taxable event, such as sale, transfer, disposal, rent, etc., of offerings for consideration in cash or kind and requires state-wise registration. While some essentials are under the 0% tax slab, there are four primary tax slabs for GST calculation and return – 5%, 12%, 18%, and 28%. It is a far cry from implementation by most other countries that have a uniform rate to ensure a seamless tax structure for a business.

In addition, companies are also liable to deduct professional tax from the salaries of their employees. The amount depends on information about professional tax applicability and the gratuities received by each salaried individual.

If any business is into importing or exporting goods, they are liable to pay customs duty to the government as an indirect tax. India follows the universally acknowledged harmonized nomenclature (HSN) classification rules that state the duty payable.

The final indirect taxation prevalent in India is known as VAT (Value Added Tax). It is only applicable today on liquor and tobacco or the product’s price and paid by the companies dealing with such offerings.

Conclusion

India has a deep-rooted structural issue where it has failed miserably in ensuring a clutter-free tax regime for corporations. The introduction of GST was a golden opportunity to set things right. On the other hand, ample rates for it brought about the same ambiguity which was quite prevalent earlier.

So, we often experience corporates, especially MSMEs, suffering from tax fatigue or the inability to handle their tax liabilities well. Therefore, there is a need to implement robust IT solutions, such as a tax-integrated payment gateway, that would enable them to handle their tax more efficiently.

PayU India offers a fully integrated, powerful payment solution provider for your offline and online presence. Moreover, it is GST-ready, so our omnichannel solution seamlessly handles most of your indirect tax needs.

Click here to get rid of your tax hassles by imbibing PayU India for your daily transactions.