AI-Powered Summary

- UPI transformed India’s payment landscape by making digital transactions more convenient and habitual, replacing cash as the default payment method.

- It digitized trust with instant confirmations and reliability, enabling seamless money transfers and reducing anxiety around digital payments.

- Small businesses gained financial visibility through QR codes, creating data trails that enabled new lending models and financial inclusion.

- India’s UPI infrastructure is now being exported globally, showcasing a population-scale digital payment system designed for inclusivity and local realities.

- The next decade of UPI will focus on integrating credit, enhancing simplicity, fostering interoperability, and leveraging transaction data for broader financial inclusion.

- UPI’s success lies in its ability to disappear into everyday behavior, setting a benchmark for infrastructure design that solves real-world challenges.

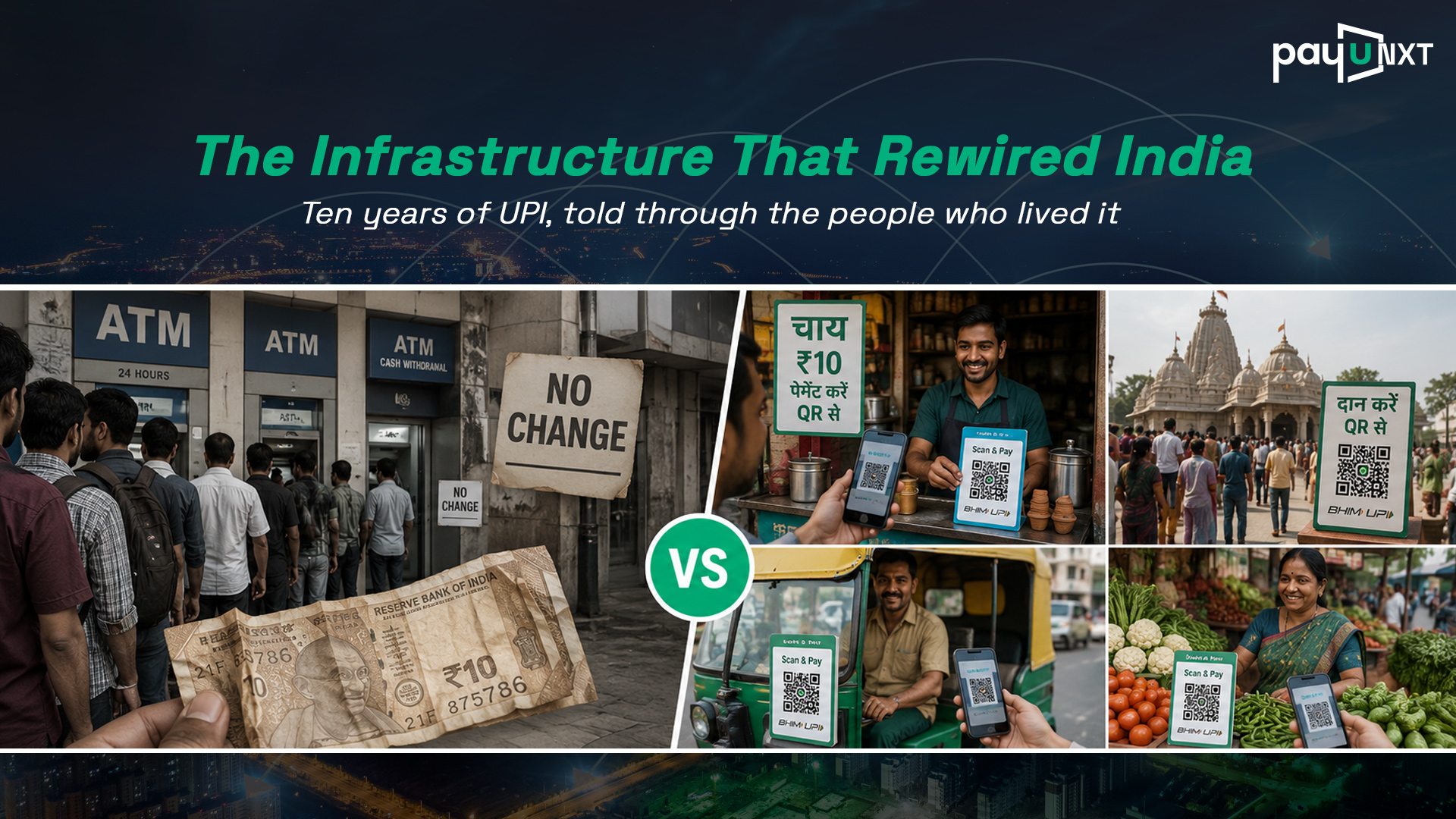

The Coconut Seller

A coconut seller on a highway outside Pune had run his business the same way for decades: cash in hand, change in pocket, no paperwork. When customers didn’t have exact change, he’d shrug. When they did, he’d smile. The system worked.

Then, almost overnight, digital payments stopped feeling optional.

A relative helped him tape a printed QR code to his cart with a rubber band. He didn’t fully understand how it worked. He just knew that when customers pointed their phones at it, a notification arrived, and the money showed up.

A few years later, that QR code became more reliable than loose cash.

And that small shift happened everywhere.

At chai stalls. At temple counters. Inside auto rickshaws. At roadside fruit carts.

UPI didn’t spread because India suddenly became tech-savvy. It spread because, for millions of people, it slowly became the easier way to transact. That’s what made it powerful.

Not marketing. Not incentives.

But

Habit. Convenience. And a technology that was, for once, genuinely easier than the alternative.

What began as a small behavioural shift at millions of counters eventually became one of the largest financial infrastructure transformations in the world.

The Scale Is Almost Absurd

India now accounts for nearly half of the world’s real-time digital payments.

At population scale, that level of adoption is almost unprecedented.

Not the US.

Not China.

Not Europe.

India.

And yet, the most fascinating part of the UPI story isn’t the scale. It’s the psychology.

The Real Revolution Happened Inside People’s Heads

Here’s the thing about technology that genuinely works: you stop noticing it.

You don’t think about electricity when you flip a switch. You don’t think about the internet when you open Instagram. And today, most Indians don’t think about UPI when they pay for chai. They just pay for chai.

That invisibility is the real achievement.

But beneath it, three things shifted in ways that are still playing out.

1. Trust got digitized

Before UPI, sending money digitally carried anxiety:

Would it arrive? Would it fail? Would there be proof?

UPI reduced that uncertainty with instant confirmations, transaction IDs, and reliability strong enough that failure became surprising.

At this scale, reliability stopped being a product feature. It became public infrastructure.

Today, people transfer money to strangers without hesitation. Digital trust, once limited to institutions, became everyday behaviour.

2. Small businesses became financially visible

For millions of kirana stores and street vendors, UPI did more than simplify payments. It created a financial trail.

Before this, a merchant’s business history often lived in notebooks or memory. There was little formal proof of income or transaction behaviour.

The QR code changed that.

Every payment became a data point. Enough data points became a financial identity. Banks and NBFCs began building entirely new lending models around this: cash-flow lending, embedded credit, revenue-based financing.

The QR code quietly became an economic passport for people who never had one.

3. Cash became the backup.

Once digital trust became habitual, something even bigger changed. Cash stopped being the default.

Ask a twenty-five-year-old in any Indian city what happens when UPI fails. They’ll refresh the app, check their signal, try again, and only then reach for cash.

Like using SMS only when WhatsApp stops working.

Cash still works. It’s just no longer the default. It’s just no longer the first choice.

The Decade That Changed Everything

Behaviour changed gradually. But a few moments dramatically accelerated the shift.

India’s Most Powerful Export Might Be Invisible

UPI is no longer just India’s payments infrastructure. It’s becoming infrastructure diplomacy.

Countries across Asia, the Middle East, and Europe are now integrating UPI rails and payment corridors. The world isn’t just studying India’s fintech growth anymore. It’s studying India’s infrastructure philosophy. And there’s a reason for that.

India didn’t copy a Western fintech playbook. It built for Indian realities:

- low-cost smartphones

- fragmented banking access

- multilingual users

- population-scale inclusion

That constraint-first thinking became India’s advantage. India may have become the first country to export population-scale digital payment infrastructure as a public good, not just enabling payments abroad, but actively building UPI-equivalent systems for other countries’ domestic use.

The Layer Consumers Never See

Most consumers only see the QR code.

Behind every successful UPI payment sits a quieter layer of infrastructure:

payment gateways, fraud systems, reconciliation engines, acquiring banks, and merchant technology that consumers rarely see. That invisible layer is where the next phase of UPI innovation is being built.

Companies like PayU have spent years building this merchant-side infrastructure:

the systems that make payments seamless, scalable, secure, and intelligent behind the scenes.

Because the next decade of UPI won’t just be about more transactions.

It’ll be about smarter transactions.

What the Next Decade of UPI Will Actually Be About

The first decade of UPI was about digitising payments. The next decade may be about digitising financial trust. A few shifts already seem underway:

1. Credit will merge into the payment layer

RuPay credit cards on UPI were just the beginning.

UPI is steadily becoming a real-time credit infrastructure layer, especially for MSMEs and new-to-credit users. Transaction history is turning into financial identity, enabling embedded credit and cash-flow-based lending.

The next major UPI story may not be payments. It may be credit.

2. Growth will come from simplicity

India has already proven digital payments can scale.

The next challenge is making them effortless – through simpler onboarding, vernacular experiences, assisted commerce, and lighter interfaces.

The next wave of users won’t care about “fintech.” They’ll care about whether it simply works.

3. Interoperability will become India’s biggest advantage

UPI succeeded because it was interoperable from day one.

As more countries build real-time payment systems, the real advantage will come from connecting them seamlessly.

The next payments battle may not be about wallets. It may be about interoperability.

4. The data layer will define the next phase of inclusion

UPI has created one of the richest streams of transaction data ever generated at population scale.

Combined with India’s broader DPI ecosystem, that data could unlock more contextual and consent-driven financial services –

from credit and insurance to investments and merchant tools.

The next phase of inclusion may be about making financial data useful, portable, and user-controlled.

Ten Years Later, Here’s What Actually Matters

UPI succeeded because it solved for India. UPI succeeded because it solved for Indian realities first.

India built population-scale digital trust. And maybe that’s the real achievement. Most technologies change habits slowly. UPI changed them within a generation.

The most successful technology products disappear into behaviour. UPI already has.

The question worth asking isn’t how far has UPI come?

It’s: what other parts of everyday life could change if infrastructure was designed this well?